We have put together some frequently asked questions, the answers to which come from a variety of sources including Revenue’s online Customs and Traders web-pages.

Frequently Asked Questions About Customs In Ireland

If you import goods from outside the European Union (EU) or if you export goods to countries outside the EU, you or your agent must complete a customs declaration. Some goods are prohibited and some are subject to restrictions or may require a licence. Goods may attract import duty and VAT.

Customs declarations must be made electronically using Revenue’s Automated Entry Processing (AEP) system.

All customs declarations for export must be lodged electronically. AEP is the system used for the completion of customs related procedures in an electronic format. The system handles the validation, processing, duty accounting and clearance of declarations to Revenue for customs purposes. The system also checks updated data format, validations and prohibitions and restrictions.

Custran enables the processing of customs declarations via a secure connection with revenues AEP system, either in-house directly, or via a Custran customs agent.

Importers, exporters or their agents need dedicated software like Custran to use ‘Direct Trader Input’ (DTI) for making electronic declarations to Revenue’s AEP system. Custran provides this software as a service to companies and customs agents.

To use Custran directly in-house, complete the application for approval for direct trader input and submit it through your ROS MyEnquiries.

You will require a digital certificate which you can get from ROS. The AEP system operates on an almost 24 hour basis.

You must register for ROS. This is a three-step process.

Step 1

Apply for your ROS Access Number (RAN). Visit the Revenue website and go to “online services” tab. Click “register for ROS” to begin the process. Click “apply for RAN”. Follow the remainder of the steps on the form to become the ROS administrator. Press submit and a RAN number will be post to your business address within 5 working days. Please watch this short video to see how to apply for a RAN number

Step 2

Apply for your digital certificate. Visit the Revenue website and go to the “online services” tab. Click apply for digital certificate. Enter your RAN number. Follow the remainder of the steps of apply for your digital cert. Watch this short video on how to apply for your digital certificate. Please watch this short video to see how to apply for a digital certificate.

Step 3

Download and save your digital certificate. Go to the Revenue website and go to the “online services” tab. Click register for ROS to start step 3 of the process. Click “download your certificate”. When prompted by ROS choose to create a backup digital certificate.

The certificate will be downloaded to your default download folder on your device. Please don’t forget your digital certificate password.

Watch this short video to see how to download and save your digital certificate.

If you use an existing digital certificate for other tax returns VAT/income tax etc. and if you register for an EORI number, then your existing digital certificate can be used, when making a customs declaration.

Every trader who interacts with customs authorities in any Member State of the EU is allocated a unique reference number called an EORI number. This reference number will be valid throughout the EU. It will serve as a common reference number for the trader’s interaction with the customs authorities of any Member State.

This number must be used by traders on all export declarations. It is also used when exchanging information between the customs authorities of the EU and between customs and other bodies for example statistical authorities.

For convenience Revenue has aligned the EORI number to the VAT number.

How does EORI work?

The EORI system has two separate and distinct elements to it, one at national or Member State level and one at EU level.

(a) National EORI system

At national level, each customs authority assigns a unique EORI number to each trader who interacts with customs. Traders must use this number in all customs declarations lodged by them or on their behalf in any Member State.

(b) Central EU EORI database

Revenue is obliged to provide details to the European Commission of all those traders who have been assigned an EORI number. These details are held on a central EU database maintained by the European Commission, which also contains similar information provided by the other 27 Member States.

Third parties can view certain limited details of all EORI registered traders (EORI number, name and address) on the central EU database. This allows a third party who is carrying out some customs activity (such as making a customs declaration) on behalf of a trader to look up the EORI number. Third parties may confirm the validity of all EORI numbers on the database.

However, third parties can only access information stored on the database where a trader has given specific consent to publication of those details.

Revenue will not publish any information on the EU database without the trader’s consent.

What should a trader who has not been assigned an EORI number do?

Any trader who hasn’t already been assigned an EORI number and wishes to export goods should contact the AEP Helpdesk, email ecustoms@revenue.ie, telephone +

353 1 738 3677 / +353 67 63139,before making the customs declaration to have an EORI number assigned.

AEO status is a certified standard authorisation issued by customs administrations in the European Union (EU). It certifies that a business has met certain standards in relation to:

• safety and security

• systems to manage commercial records

• compliance with customs rules

• financial solvency

• practical standards of competence or professional qualifications.

This is primarily a trade facilitation measure that recognises reliable operators and encourages best practice in the international supply chain.

Application for AEO status is open to all economic operators established within the customs territory of the EU. Article 5 (5) of the Union Customs Code defines an economic operator as a ‘’person who in the course of his business, is involved in activities covered by the customs legislation’’.

AEO status is open to all links in the global supply chain that is manufacturers, exporters, freight forwarders, warehouse-keepers, clearance agents, carriers and importers.

However, there are four sets of criteria, which must be satisfied, as follows:

• an appropriate record of compliance with Revenue requirements

• a satisfactory system of managing commercial and, where appropriate transport records which allow appropriate Revenue controls

• proven financial solvency

and

• appropriate security and safety standards.

• AEOs may lodge export declarations using the reduced data requirements with regard to safety and security.

• AEOs are recognised worldwide as safe, secure and compliant business partners in international trade.

• AEOs are given a lower risk score in risk analysis systems when profiling.

• If physical controls are to be conducted, AEOs will be given priority treatment.

• Mutual recognition of AEO programs under Joint Customs Co-operation

Agreements can result in faster movement of goods through third country borders.

• AEOs are in a stronger position to benefit from simplified procedures.

Because AEO traders have increased safety and security standards they may also benefit from:

• reduced theft and losses

• fewer delayed shipments

• improved planning

• improved customer loyalty

• reduced security and safety incidents

• reduced crime and vandalism

• improved security and communication between supply chain partners.

How do you apply for AEO status?

Before you apply for AEO status you should complete this self-assessment questionnaire. This will help you to evaluate your procedures and ensure they meet the criteria for AEO. The explanatory notes for the self-assessment questionnaire will help you to complete this questionnaire.

Importers, exporters or their agents need dedicated software to use DTI for making electronic declarations to the Automated Entry Processing system (AEP). In the absence of this software you can appoint a customs agent to make declarations on your behalf.

To apply for this facility you should complete the application for approval for direct trader input and submit it through MyEnquiries.

DTI users communicate with the AEP system through Revenue Online Service (ROS). You will require a digital certificate which you can get from ROS. The AEP system operates on an almost 24 hour basis.

You will find further information about DTI in the AEP trader guides.

Export is one of a number of customs procedures for dealing with goods. Each of the procedures has its own rules. If you wish to use a procedure you must formally make a declaration to Revenue for that purpose.

What is an export declaration?

An export declaration for customs purposes is the legal act, whereby a person indicates a wish to place goods under the export procedure.

How do you make an export declaration?

You must lodge your customs declaration electronically, using Revenue’s Automated Entry Processing (AEP) system, which is described later in this guide. The customs declaration gives all the information needed about what the goods are and what is happening to the shipment. The declaration contains 54 boxes, but only some of them must be completed. You will find information about which boxes to complete and why in the AEP trader guides.

Revenue will require an export declaration if you:

-

- export goods to a non-EU country

- export goods to the special territories of the EU which are part of its customs territory but are not part of its fiscal territory

- export CAP goods to an entitled destination under the provisions of Commission Regulation (EEC) No. 612/09

- deliver goods tax exempt as aircraft and ship supplies, regardless of the

destination of the aircraft or ship.

You do not have to make an export declaration for goods of Irish or EU origin which are in free circulation in Ireland that are being dispatched to other EU Member States.

Types of Export

There are three types of export:

• Direct exports – goods leave Ireland directly for their destination outside the

EU.

• Indirect exports – goods leave Ireland, travel to one or more other Member

State(s) and leave from there for a destination outside the EU.

• Exports made under a Single Transport Contract – in this case the goods leave Ireland and travel to one or more other Member State(s) from which they leave for their destination outside the EU (in the same way as indirect exports).

However, they are treated as if they are direct exports and all customs formalities are completed in Ireland at the request of the declarant.

An export declaration containing specific items relating to safety and security requirements must be lodged, using the AEP system, in advance of an export movement. The exact time of lodgement depends on the nature of the cargo and how the export is being affected.

The person responsible for lodging the export declaration is the exporter, that is the person who has the power for determining that the goods are to be brought to a destination outside the customs territory of the Union and who may hold a contract with the consignee outside of the Union. As stated previously, you may appoint a representative to act on your behalf.

If the entity that has the power for determining that the goods are to be brought out of the Union is not based within the Union, then an indirect representative may be appointed to act on your behalf.

When your customs declaration has been accepted by the AEP system (see information in Section 5) you will be notified of the routing for your goods. There are three different routings, green, orange and red and the characteristics of each are as follows:

• Green Routing – indicates that your goods have been cleared by Revenue on the basis of the export declaration received.

• Orange Routing – indicates that your goods have been selected for a documentary check and you must furnish Revenue with all relevant documents, before your goods can be cleared. If everything is in order Revenue will finalise the export declaration on the AEP system.

• Red Routing – indicates that your goods have been selected for a documentary check and a physical examination. Revenue will check to ensure that the goods declared on the export declaration correspond to the actual goods. If everything is in order Revenue will finalise the export declaration on the AEP system.

AIS release date has been put back to November 23 rd, 2020. You cannot submit a SAD import to Revenue after November 23rd.

From this date forward all import declarations will have to be AIS. There is no exception to this. The same tariffs, TARIC codes, duties and VAT apply to declarations made through AIS as declarations made through SAD import.

AIS declarations cannot be made directly to Revenue through revenue.ie or through ROS.

All AIS declarations have to be made through third party software platforms like Custran.

AIS is defined by data elements separated into 8 categories rather than boxes in a SAD.

The single administrative document (SAD) is a form used for customs declarations in the EU, Switzerland, Norway, Iceland, Turkey, the Republic of North Macedonia and Serbia. It is composed of a set of eight copies each with a different function.

Using one single document reduces the administrative burden and increases the standardisation and harmonisation of data collected on trade.

Read more on the presentation and use of the form here.

Where is the Single Administrative Document used?

-

- In the EU, the single administrative document is used for trade with non-EU countries and for the movement of non-EU goods within the EU.

- Since the 1987 Convention on the simplification of formalities in trade in goods, it also applies to the territories of the EFTA countries (Switzerland , Norway and Iceland), Turkey (since 1 December 2012), to the Republic of North Macedonia (since 1 July 2015) and to trade between these countries and the EU.

- Finally, it remains applicable in certain extremely limited cases of movement of EU goods inside the EU (for example: possible individual measures for the period of transition following the accession of new Member States, trade with parts of the customs territory of the EU which are not part of the fiscal territory of the Member States).

Procedures covered

The document covers the placement of any goods under any customs procedure such as: export, free circulation, transit (where the New Computerised Transit System was not used), warehouses, temporary admission, inward and outward processing, etc.

For more see ec.europa.eu

Revenue may require exporters to produce transport documents, licences or documents relating to the previous customs procedure when the export declaration is orange-routed or red-routed by AEP.

All documents must be retained for the purpose of post-clearance checks for a period of three years from the end of the year in which an export takes place. Where a single item is presented in two or more packages, Revenue may also request a packing list or equivalent document indicating the contents of each package.

An export licence is a document issued by the relevant government department authorising the export of restricted goods. An export licence may be needed for any goods and can range from live animals and animal products to endangered species and cultural goods. The export of ozone depleting substances, dual-use goods, arms and ammunition and other military goods are also controlled. A Common Agricultural Policy (CAP) licence will probably be required whenever an export refund is being claimed.

How do you know if you need a licence?

You should check your goods on TARIC to see if a licence is required. As licences are required for a range of items, you could also check with the relevant government department as to whether one is required.

The following licences are those commonly required for exports:

• CAP licences are usually needed for the export of foodstuffs, whether as raw materials or processed products. They are issued by the Department of Agriculture, Food and the Marine and controlled by Revenue. The Department of Agriculture, Food and the Marine will be able to tell you if a licence is required. Their general contact number is +353(0) 1 607 2000 or 076 1064 400, or you can visit their website at www.agriculture.gov.ie. If a licence is required and is not presented at the time of export, the consignment will not be

released for export. You should note that the country of destination is a factor in whether or not a licence may be required. CAP goods declared for one country of destination may need a licence, whereas the same consignment going to another country may not.

• An export licence from the Department of Business Enterprise and Innovation may be needed for the export of:

o military, security and paramilitary equipment, firearms, ammunition, explosives and related goods to all destinations, including other EU Member States

o dual-use goods (a wide range of civil goods that can have a military application) to destinations outside the customs territory of the Union

o highly sensitive dual-use goods to all destinations, including other EU Member States

o goods that you are aware, or about which you have been informed, may be for use in connection with chemical, biological or nuclear weapons

o goods being exported to countries that have UN, EU or OSCE (Organisation for Security and Co-operation in Europe) sanctions currently imposed against them.

In addition, many less sensitive goods being exported to less sensitive destinations may be covered by a global export licence. You can contact the Department of Business, Enterprise and Innovation, export licencing unit on + 353 1 631 2121, or visit Market Access Database for further information. If a licence is required and is not presented, the goods may be seized.

• A licence from the Department of Culture, Heritage and the Gaeltacht is required for the export of certain cultural or heritage items from Ireland. You can contact the Department of Culture, Heritage and the Gaeltacht (Cultural Institutions Unit), New Road, Killarney, Co. Kerry on + 353 64 662 7300 or visit their website: Department of Culture, Heritage and the Gaeltacht for further information.

The commodity code used for exports is a ten-digit number. This corresponds to a description of the item. Every product has a unique commodity code. A commodity code is required on all normal export declarations. It is entered in box 33 of the customs export declaration. Commodity codes are set out in TARIC.

TARIC, is a database managed by the European Commission and used by all Member States. It is updated daily and has a simulation date facility, which allows the user to search for a rate of duty on any given date.

In TARIC you will find information about:

• classifying your goods

• commodity code numbers

and

• rates of duty for any date that you may enter.

You can use TARIC to classify your goods by using:

• the description – typing in the description of the goods

or

• by using the browse facility – viewing all sections or chapters.

It is important to keep up-to-date with changes in commodity codes, rates of duty

and regulations related to your products.

If after studying TARIC you are unable to classify your goods for customs purposes or have queries regarding the classification of your goods, you can contact Classification, Origin and Valuation Unit. This Unit will offer an opinion on the classification of your product.

You can also apply for a Binding Tariff Information (BTI), which is a tariff classification decision that is legally binding throughout the EU.

Contact details for Classification, Origin and Valuation unit:

• telephone – + 353 1 738 3676 9:15 to 17:00 Monday to Friday (except Public

Holidays)

• Address – Customs Division, Government Offices, St. Conlon’s Road, Nenagh,

Co. Tipperary, E45 T611.

• MyEnquiries

BTI is an EU-wide system that provides traders with tariff classification decisions that are legally binding throughout the EU. BTI decisions are issued by the customs administrations in the various Member States.

The BTI database may be accessed at the following link – BTI Database.

What are the benefits of BTI for Traders?

The benefits of BTI for traders are as follows:

• Legal certainty regarding tariff classification decisions.

• The rules of classification are applied uniformly throughout the EU.

• BTI may be invalidated due, for example, to a change in EU legislation. If approved, traders may be allowed a period of grace to complete any binding contracts entered into on the basis of that BTI.

• Revenue will advise traders if any classification changes occur that affect their BTI.

How do you obtain a BTI?

You should send your completed BTI application form by:

• post to:

Classification, Origin and Valuation Unit

Customs Division

Government Offices

St. Conlon’s Road

Nenagh

Co. Tipperary

E45 T611

• MyEnquiries

The customs procedure code describes the procedure or the economic regime under which the goods are to be exported. It is required on all export declarations and should be entered in Box 37 of the customs export declaration. A list of procedure codes for exports can be found in appendix 18 of the AEP Trader Guide.

Usually goods are exported as a result of a straightforward sale to a customer overseas.

However, there can be a number of other reasons why goods are exported including:

• goods going out on long-term loan or hire, to be returned eventually

• goods being temporarily exported for repair

• goods being re-exported after processing by an Irish or EU company.

Goods that are exported temporarily may be eligible for relief from duty when they are re-imported to Ireland or the EU. You must, however, inform Revenue of this at the time of exporting the goods. You can do this by using the appropriate customs procedure code. You cannot apply for this retrospectively.

It is important to use the correct customs procedure code when you declare your goods for permanent export. If you are VAT registered your customs declaration with the correct procedure code forms part of your evidence to support zero rating of the transaction.

It is the legal requirement of the importer of the goods to select the correct classification code for the goods post-Brexit. The correct commodity code is required by customs to ensure that the correct duties are paid on the imported goods. The specific commodity code will inform customs if subsequent checks have to be made on goods at the port, for instance anti-dumping or possible tariff suspension.

Customs duties will apply to imported goods in the UK post-Brexit and the UK will no longer utilizes the EUs TARIC to determine duty rates. The UK has introduced a “Trade Tariff Look Up” for traders who wish to find information on commodity codes and import duties applicable in the UK. See more here.

An import commodity code is a 10-digit code. The first 6 digits are from the global harmonised system. These 6-digit codes are common to the same goods throughout the world. Digits 7 and 8 are international identifiers unique to every country.

To identify the correct commodity code, follow these steps.

Select browse button on TARIC available here.

Select your section and then your chapters.

Check the legal notes that go with each commodity code. These notes are renewed every year.

Your product must comply with the heading text. Your heading is the first 4 digits in your commodity code.

Your product must legally comply with the wording of the heading

Continue to subheading text to try and narrow the search.

Your product must comply with these subheadings

You will have to consider the “essential character” of the goods when classifying and selecting your code, as certain products will not always fit neatly into the sections and chapters of TARIC.

If you are importing a novel product and you are having great difficulty with the classification of the goods, consult an expert. You may need to consider using the Binding Tariff Information (BTI). For more information on BTI and other commodity code related issues, click here.

The method used is the Free On Board (FOB) method. This value is established by calculating the cost of the goods to the purchaser abroad, adjusted as follows:

The following should be included:

• export charges, if any, payable by the exporter arising from the export of the goods from Ireland, for example CAP charges or disease eradication levies

• costs, profits, expenses and so on, accruing up to the point of delivery of the goods on board the exporting ship or aircraft such as:

o packing costs

o inland freight charges

o dock dues

o loading and handling charges

o customs clearance charges

o all other costs profits and expenses, including insurance and commission.

The following should be excluded:

• Freight charges, transport insurance charges and so on, payable to transport the goods beyond the port or place of export from the State.

• Any sum receivable by the exporter by way of export refund or subsidy. If for example, a live animal valued at €500 is being exported to a non-EU country and the Department of Agriculture, Food and the Marine pays an export refund of €200, the value to be declared is €300.

• Any foreign Customs Duty payable on the goods after they are exported from the EU.

Any cash discounts and trade discounts granted to the purchaser abroad should also be deducted. The value of the goods should be entered in Box 46 of the customs export declaration.

The effective date for the export procedure is the date of acceptance by Revenue of the declaration. The goods must not be removed from the place of presentation until released by Revenue. The goods remain under Revenue supervision until they leave the customs territory of the EU. The date of acceptance is important because of the effect it can have on any export charges or refunds or on licensing requirements that may be in place.

Yes. A declarant may be authorised to amend one or more of the details on the declaration after it has been accepted by Revenue. However, the amendment cannot have the effect of applying the declaration to goods other than those it originally covered. However, it should be noted that no amendment is permitted after

Revenue has:

• informed the declarant that they intend to examine the goods

• established that the particulars in question are incorrect

or

• released the goods for export.

An export declaration should normally be lodged using the AEP system to the customs office:

• responsible for supervising the place where the exporter is established

or

• where the goods are packed or loaded for export shipment.

However, there are exceptions to the normal procedure above and where, for administrative reasons it cannot be applied, the declaration may be lodged:

• to any customs office in Ireland, which is competent to deal with the export procedure concerned

or

• in another Member State where there are duly justified good reasons, as described in the following paragraphs.

Duly justified good reasons exist where the lodgement of a declaration at the normal customs office would require an economically unreasonable effort by the exporter and may include the following:

• a change of contract

• diversion of goods

or

• loss of documents.

Duly justified good reasons do not exist:

• in cases where the place for lodging a declaration through normal procedures is closed when the goods are about to be shipped

or

• where a significant economic advantage accrues to the exporter by lodging the export declaration in another Member State in cases where agricultural refunds are due

When exporting, the declarant should print the Export Accompanying Document (EAD) and this should accompany the goods on their movement to the other Member State. The function of the EAD is to show that an export declaration has been lodged and the shipment has been released for export.

The customs office of export will send a message to the office of exit that the goods are on their way. On arrival of the goods at the office of exit, the EAD should be presented to customs by the declarant or agent working on his behalf.

The customs authorities in some Member States may require notification of arrival of the goods at the customs office of exit to be communicated to them electronically. This will allow customs in the office of exit to supervise the physical exit of the goods from the EU and also to inform the office of export in Ireland that exit has taken place.

ECS is an IT system that has been introduced throughout the EU for the control of indirect exports. These are goods that are exported from one Member State (office of export) but that exit the EU through another Member State (office of exit).

An example of an indirect export is where goods leave Dublin, are flown to Paris and are then flown onwards to the United States. In this scenario, Ireland is the country of export and Dublin Airport is the office of export. France is the country of exit and Charles De Gaulle Airport in Paris is the office of exit. Irish and French customs communicate electronically with each other using ECS in relation to this indirect export.

How does ECS work?

Where an export declaration is lodged to AEP and Box 29 shows the office of exit to be in another Member State (you will find office of exit codes in EUROPA COL list) the export movement will be automatically processed though ECS. AEP generates a Master Reference Number (MRN) (see below) which is notified electronically to the declarant and can be reproduced in both numeric and barcode formats.

The declarant should print the Export Accompanying Document (EAD) and this should accompany the goods on their movement to the other Member State. The function of the EAD is to show that an export declaration has been lodged and the shipment has been released for export.

The customs office of export will send a message to the office of exit that the goods are on their way. On arrival of the goods at the office of exit, the EAD should be presented to customs by the declarant or agent working on his behalf. The customs authorities in some Member States may require notification of arrival of the goods at the customs office of exit to be communicated to them electronically. This will allow customs in the office of exit to supervise the physical exit of the goods from the EU and also to inform the office of export in Ireland that exit has taken place.

The declarant in Ireland will receive a further message from AEP confirming that the goods have exited from the EU.

Traders who wish to obtain more information in relation to ECS can contact the AEP helpdesk at Tel. +353 1 738 3677 / +353 67 63139 or by email at ecustoms@revenue.ie

Outward processing is a customs procedure which allows EU goods to be temporarily exported from the customs territory of the EU in order to undergo processing operations or repair. You can claim full or partial relief from import charges when these goods are re-imported and released for free circulation in the EU.

Outward processing allows businesses to take advantage of more competitive labour costs outside the EU. It also encourages the use of EU produced raw materials to manufacture the finished products. You can also temporarily export goods to undergo processes not available within the EU.

Outward processing is granted only to natural or legal persons established in the EU. You will require an authorisation and must be the person carrying out the process or arranging for it to be carried out.

Outward processing cannot be used for EU goods:

• if their export gives rise to a refund or remission of import duties

• that before export, are released for free circulation free of import duties because of their use for particular purposes, if the conditions for granting that relief continue to apply

• if their export gives rise to export refunds or other amounts under the Common Agricultural Policy

• for which a financial advantage is granted because of their export.

You should make your application for outward processing electronically using the Customs Decisions System (CDS).

The NCTS allows you to submit and finalise your transit declarations by electronic means. The following countries can use NCTS:

Member States of the European Union (EU)

European Free Trade Association (EFTA) countries

Turkey

The Republic of North Macedonia

and

Serbia.

You can connect into the NCTS system through Revenue’s Online Services (ROS). Once you are connected you can:

-

- generate electronic transit messages

- send or receive messages to and from the IRL – NCTS

- receive electronic replies, such as acceptance of declaration, release of goods and notification of discharge.

For further information, see NCTS Traders Guide – Guide to assist traders in the use of NCTS.

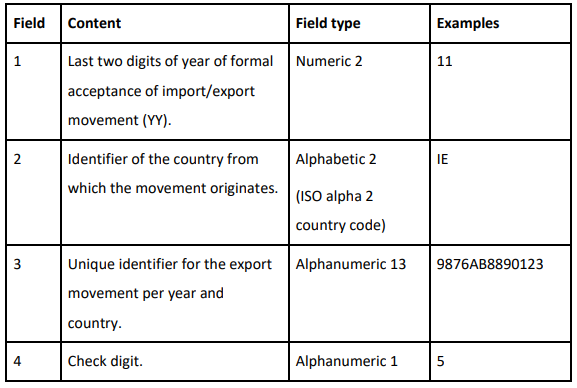

The MRN is a unique number that is automatically allocated by AEP when it receives and validates the export declaration.

It contains 18 digits and is composed of the following elements:

A STC may also be referred to as:

• a through bill of lading (for maritime)

or

• a through air waybill (for air freight).

It is used where the commercial contract for the carriage of the goods is end-to-end. An example of this would be where an exporter makes a booking with a freight forwarder to export goods from Dublin to Shanghai. The export will not move directly between these locations. The goods may be moved using various modes of transport (including by road) through any route determined by the freight forwarder or ocean carrier. The exporter or declarant may not be aware of the exact route. It is not possible to request STC where the final exit from the EU is to be made by road.

When STC is requested, it allows the Irish customs office to operate as both office of export and office of exit. As a result the formalities of the office of exit are completed here in Ireland before the export starts its journey.

ATA carnets are instruments, which may be used to simplify customs clearance of goods being temporarily exported for a specific purpose for example:

• for displays

• exhibitions and fairs

• professional equipment

• commercial samples.

The ATA carnet replaces normal customs declarations at export and re-import. They also replace normal customs documents and security requirements in many countries worldwide into which the goods are being temporarily imported.

Goods covered by ATA carnets are subject to normal export prohibitions and restrictions and licensing rules.

The carnets may not be used for goods that are:

• exported for process or repair

• exported by post

• not in free circulation before export from the EU.

The Dublin Chamber of Commerce issues ATA carnets in Ireland. A guarantee or a deposit from the exporter will be required.

The importer of the goods is responsible for paying the monies for duties and VAT to revenue. The trader is ultimately responsible for the correct selection of the commodity code used for the imported goods. The importer must also keep a record of their declaration’s history in case of an audit from revenue. An importer must set up a Trader Account Number (TAN) account in order to pay duties, VAT, Vehicle Registration Tax (VRT) or excise duty. Even if the duty is at zero on imported goods a trader is obliged to set up a TAN account. This is in case of an audit where monies may have to be paid retrospectively. For information on how to set up a TAN account please contact revenue.

You can also apply for deferred payment to revenue. The deferred payment system (bank direct debit scheme) is an authorisation that allows you to defer payment of certain charges. These charges include Customs Duty, VAT at import, Excise Duty and VRT. You must lodge a guarantee and comply with the conditions of the authorisation. The authorisation allows you, once approved, to pay the duties and taxes due by direct debit in the following month. Excise traders operating from a warehouse must operate on a deferred basis only.

The most convenient way to keep your TAN account topped up is to use revenue’s RevPay. This is a digital service whereby the trader inputs their credit/debit card details into RevPay, and they can make a transfer to their TAN account. This method of top up is an instant transfer of funds to the TAN account.

Traders can also apply to revenue for deferred payment status. This status permits the trader to defer the payment of VAT or duties owing until the middle of the following month. You must also apply to revenue for a comprehensive guarantee.

You can re-import goods that were originally exported from the EU and qualify for relief from the payment of Customs Duty and Value-Added Tax. This is called returned goods relief. The goods must be re-imported within three years from the date of export and must be in the same condition as when they were exported in order to qualify. Returned Goods Relief can be used if your overseas customer needs to return goods to you, that is if they are damaged or are not what they originally ordered.

How can you obtain Returned Goods Relief?

You do not need an authorisation to obtain Returned Goods Relief. In order to support your claim for Returned Goods Relief, you must be able to prove to Revenue that the goods were originally exported from the customs territory of the EU. You must also establish their “duty status” at the time of original export, that is whether or not the goods were originally imported to the EU at a reduced or nil rate of duty because of their use for a particular purpose for example under the end-use procedure.

Further information

You will find further information:

• in Goods re-imported into the European Union on the Revenue website

• by contacting the Authorisations and Reliefs Unit, Customs Division, Government Offices, St. Conlon’s Road, Nenagh, Co. Tipperary, E45 T611. Telephone: + 353 1 738 3676

• by email at customsreliefs@revenue.ie.

Goods may be seized by Revenue if there is evidence that a false declaration has been knowingly made. Seized goods may be validly claimed by the person from whom they have been seized, or by their owner, or by a person authorised by him or her.

To be valid, a claim must:

• be made within one calendar month from the date of seizure

• be made in writing

• be addressed to the officer who seized the goods or to the District Manager in whose area the goods were seized or, to Revenue, Investigations and Prosecutions Division, Áras Áiligh, Bridgend, Co. Donegal

• clearly state the claimant’s full name and address.

If the address of the claimant is outside of Ireland, the claimant must give the name and address of a solicitor practising in Ireland who is authorised to accept service of any legal documents on his or her behalf.

When a valid claim is received, Revenue may:

• offer settlement terms or

• institute legal proceedings for the forfeiture of the goods. If a valid claim is not received, the goods are by law deemed to be forfeit to the State and Revenue may dispose of them.

When an excise offence is committed, in addition to seizure of the goods, the offender is liable to prosecution.

Where Revenue proposes to take a decision that will adversely affect a person (for example a refusal of an authorisation), that person must be given an opportunity to express their point of view before the decision is taken. This principle is known as “right to be heard”.

Where this principle is availed of and the decision remains the same, it may be appealed.

In such an event, Revenue will inform the person affected of this fact and outline the appeal procedures to him or her at the time of refusal.

When making an appeal you should set out in writing the basis for your appeal. You should enclose the related documents and forward it to the person from whom you have received the written decision within 30 days of that decision. You should note that the lodging of an appeal does not suspend the collection of customs debt. You will find further information about appeals in Customs appeals on the Revenue website.